Historical Options Replay for Event Studies

Daniel Ratke

Research & Engineering

Historical Options Replay for Event Studies

A historical options event replay should define the event timestamp, rebuild the contract universe with as_of, shortlist before looking at outcomes, use bid/ask quotes for fills, use trades for activity validation, and publish rejects.

Term map

Backtesting vocabulary for this article

Treat signal timestamp, point-in-time universe, quote-aware fill, reject reason, replay artifact, walk-forward test, and cache key as first-class terms. They separate reproducible research from a backtest that only preserves the final performance table.

Follow the linked definitions for Point-in-time contracts, Quote-aware fills, Reject reasons, Replay artifact, Cache key, Signal timestamp, Look-ahead leakage, Walk-forward test, Slippage model, Same-bar fill, Promotion gate, and Options data API.

Event studies are where sloppy options data assumptions become obvious. Earnings releases, Fed decisions, CPI prints, product launches, biotech catalysts, and index rebalance days create clean stories. The stock moved. The option chain repriced. IV changed. Volume appeared. It is tempting to turn that into a simple "calls won" or "puts lost" article.

The better question is more technical: what did the market actually show before the event, which contracts were listed, what bid/ask quotes were available, what trades printed, and which rows should be rejected?

This guide turns the Historical Options Data API, contracts docs, quotes docs, trades docs, and historical options replay runbook into an event-study workflow.

Define the event timestamp

The event timestamp is not the whole study. It is the anchor. For earnings, it might be the release time or first tradable session after the release. For a stock strategy, it might be the bar close that created the signal.

Record:

- event source

- event timestamp

- pre-event observation window

- entry window

- exit window

- underlying price reference

- allowed expirations or DTE bucket

- fill policy

- reject policy

If you cannot define the timestamp windows, the event replay will drift into hindsight.

Rebuild the contract universe

The replay should not begin by typing an OCC symbol from memory. Use listed expirations, then contracts with as_of.

curl "https://api.cutemarkets.com/v1/tickers/expirations/NVDA/" \

-H "Authorization: Bearer YOUR_API_KEY"

curl "https://api.cutemarkets.com/v1/options/contracts/?underlying_ticker=NVDA&as_of=2026-05-20&expiration_date.gte=2026-05-22&expiration_date.lte=2026-06-19&limit=100" \

-H "Authorization: Bearer YOUR_API_KEY"

This protects the study from future-listing leakage. It also keeps adjusted contracts, weekly dates, monthly dates, and exact OCC identifiers visible.

For more detail, link the research note to point-in-time option contract selection, backtest options without stale contracts, and option symbols and contract identity.

Shortlist without cheating

The shortlist should be created before looking at post-event winners.

Useful shortlist rules:

| Rule | Reason |

|---|---|

| DTE range | Connects the contract to the event horizon |

| Moneyness band | Prevents arbitrary far-wing selection |

| Delta band | Keeps risk profile comparable |

| Minimum open interest | Avoids empty lines |

| Minimum volume | Confirms event participation |

| Maximum spread percent | Controls execution drag |

| Quote freshness | Avoids stale bid/ask context |

| IV present | Allows volatility-crush analysis |

The options chain API is useful for current candidate selection. For historical events, use historical options data and as_of contract discovery first.

Use quotes for fills

For every selected contract, pull quotes around the entry and exit windows.

curl "https://api.cutemarkets.com/v1/options/quotes/O:NVDA260522C00180000/?timestamp.gte=2026-05-20T19:40:00Z×tamp.lt=2026-05-20T19:50:00Z&limit=1000" \

-H "Authorization: Bearer YOUR_API_KEY"

Quote-aware terminology matters here:

- bid

- ask

- midpoint

- spread dollars

- spread percent

- quote age

- displayed size

- no-bid exit

- stale quote

- quote window

The why option quotes matter more than last price post explains the core reason. Around events, the last price can be stale because the chain reprices faster than every contract prints.

Use trades for activity validation

Trades show what printed:

curl "https://api.cutemarkets.com/v1/options/trades/O:NVDA260522C00180000/?timestamp.gte=2026-05-20T19:40:00Z×tamp.lt=2026-05-21T14:00:00Z&limit=1000" \

-H "Authorization: Bearer YOUR_API_KEY"

Use trades to answer:

- did the contract print near the event?

- were prints clustered before or after the release?

- was the trade size meaningful?

- do trade prices agree with the quote window?

- does tape activity support or contradict the chain rank?

Do not use trade prints as automatic fills. That shortcut is one reason event-study backtests overstate edge.

Report IV crush beside execution quality

An event study often talks about implied volatility crush. That is useful, but IV alone can mislead. Report IV beside the fields that decide tradability.

| Metric | Why |

|---|---|

| Pre-event IV | Measures event premium before the catalyst |

| Post-event IV | Measures volatility repricing |

| Entry bid/ask | Shows cost to enter |

| Exit bid/ask | Shows exit market |

| Spread percent | Captures execution drag |

| Quote age | Rejects stale markets |

| Open interest and volume | Provides participation context |

| Reject reason | Explains missing or unusable rows |

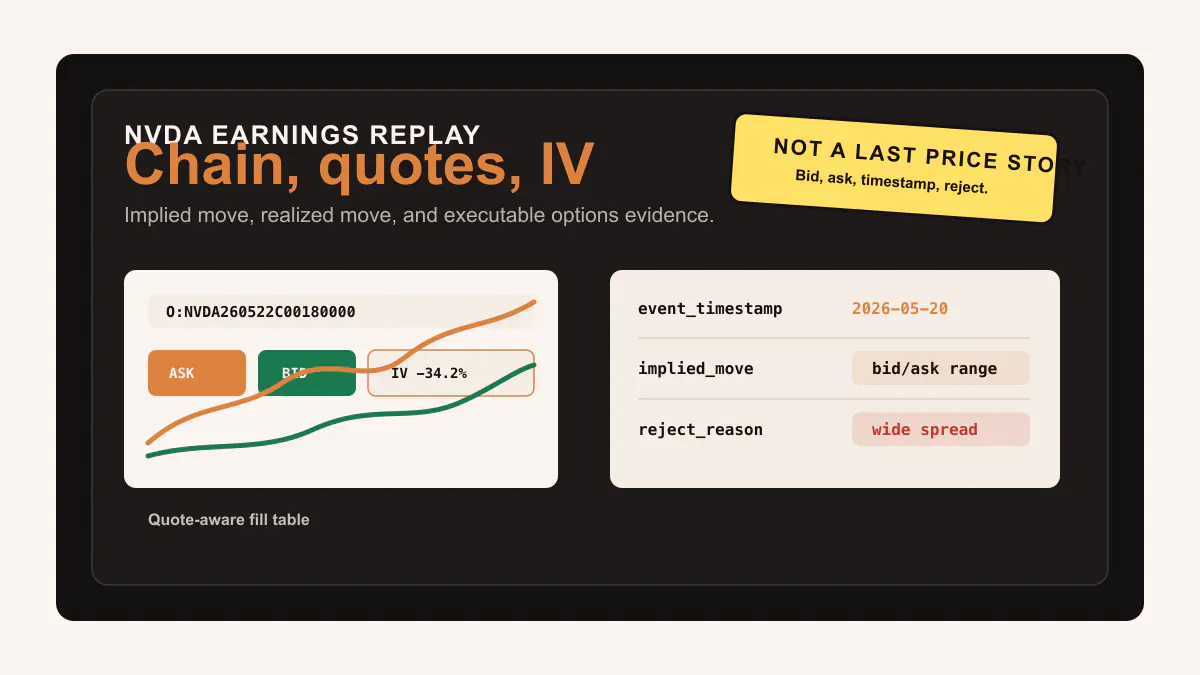

This is how the NVDA earnings replay and earnings options plays style of content becomes reproducible rather than narrative-only.

Publish the reject table

Rejects make the study more credible.

| Reject reason | Example |

|---|---|

| Contract not listed | OCC ticker did not exist at the decision date |

| Missing quote | No bid/ask rows inside the entry window |

| Stale quote | Latest quote exceeded max quote age |

| Wide spread | Spread percent exceeded policy |

| Zero bid | Exit side had no usable bid |

| Missing IV | Volatility-crush analysis required IV |

| Incomplete chain | Pagination did not load the full selected surface |

The backtesting data quality checklist, execution realism docs, and options slippage calculator all connect to these reject categories.

The conclusion should be a standard

A strong event-study article should not end with a trade recommendation. It should end with a research standard:

- exact contracts, not ticker-level ideas

- listed expirations, not guessed calendars

- quotes for fills, trades for activity

- IV beside spread and quote age

- rejected rows kept visible

- request URLs preserved

That is the subject area CuteMarkets should own: quote-aware, contract-aware, timestamp-aware options replay.

How the terminology applies

For Historical Options Replay for Event Studies, the backtesting workflow should treat Point-in-time contracts, Quote-aware fills, Reject reasons, Replay artifact, Cache key, and Signal timestamp as operational state rather than glossary decoration. That framing keeps the research claim causal: the strategy can only select instruments, prices, and labels that existed at the decision time.

A developer implementing this Deep Dive idea should persist Look-ahead leakage, Walk-forward test, Slippage model, Same-bar fill, Promotion gate, and Options data API beside the result, instead of leaving those words in a term card. It also turns attractive performance into an auditable record where fills, skips, thresholds, and replay inputs can be challenged independently.

The review artifact for Historical Options Replay for Event Studies becomes more useful when OPRA-originating data, OCC option symbol, Bid/ask spread, Midpoint, Quote/trade condition, and Quote vs trade semantics appear in the same body of evidence as the selected rows. When a result is promoted, these fields should appear in the run manifest, rather than a prose summary or final equity curve.

In production notes for this backtesting workflow, REST snapshot, WebSocket stream, Entitlement gate, Quote freshness, Timestamp semantics, and Pagination cursor define the checks that decide whether the workflow is reproducible. The result is a backtest that can be rerun, compared across threshold families, and rejected when the evidence is not strong enough.

For Historical Options Replay for Event Studies, the practical acceptance test is simple: another developer should be able to read the body, identify the exact inputs, reproduce the request sequence, and explain the accepted and rejected rows without relying on the bottom terminology grid. If a phrase appears in the page vocabulary, it should correspond to a stored field, a validation check, a replay step, or an implementation decision in the backtesting workflow.

This is also the reason the article should not measure success only by the final chart, table, or headline metric. The better standard is whether the data path, timing model, entitlement state, and evidence trail survive review. When those pieces are written directly into the body, the terminology becomes part of the workflow readers can implement.

Event replay needs two clocks

An event study should keep the event clock separate from the market-data clock. The event clock says when the earnings release, macro print, filing, or news item became observable. The market-data clock says which chain snapshot, quote row, trade row, and aggregate bar existed before or after that event. Mixing those clocks is a quiet form of look-ahead leakage.

The replay artifact should include event timestamp, market session, underlying ticker, point-in-time contract request, selected OCC option symbol, DTE bucket, strike, right, implied volatility, Greeks, open interest, NBBO quote, quote condition, trade condition, and top-of-book size. If the event window spans a close or half-day, keep the session label and timestamp semantics explicit.

For provider-style discipline, store the endpoint, dataset, response envelope, pagination cursor, and cache key for every historical window. A replay that cannot rebuild the same quote window from those fields is not ready to support a conclusion about IV crush, gap risk, or post-event drift.

Terminology

Market-data terms used in this article

These terms keep the article connected to the CuteMarkets knowledge base and to the exact API workflow behind the research.

Point-in-time contracts

Contract discovery anchored to the research date so a backtest does not use future listings.

Quote-aware fills

Entry and exit assumptions based on bid/ask quotes, quote age, spread width, and side-specific fill rules.

Reject reasons

Logged explanations for skipped contracts or fills, including stale quote, wide spread, no bid, or missing data.

Replay artifact

The saved request, selection, fill, reject, and metric record that lets another developer audit the backtest.

Cache key

The structured identifier that keeps provider, endpoint, ticker, timestamp, plan, and schema state from being mixed.

Signal timestamp

The exact time a strategy made a decision, used to reconstruct the visible universe and quote window causally.

Look-ahead leakage

A research error where a fill, contract, indicator, or label uses information unavailable at decision time.

Walk-forward test

A validation method that repeatedly trains and evaluates across separated time windows instead of trusting one optimized sample.

Slippage model

A fill-cost assumption based on bid/ask side, midpoint, spread percent, quote age, and liquidity policy.

Same-bar fill

An intraday backtest assumption that can become invalid when signal, entry, stop, and target ordering is ambiguous.

Promotion gate

The written threshold that decides whether a research candidate can move into paper trading or production monitoring.

Options data API

The product surface for chains, contracts, quotes, trades, aggregates, Greeks, IV, open interest, and expirations.

OPRA-originating data

The U.S. listed-options source context behind quotes, trades, exchange participation, and consolidated option-market records.

OCC option symbol

The exact option contract identifier that preserves root, expiration, call or put side, and strike.

Bid/ask spread

The execution interval between bid and ask that determines whether a contract is realistically tradable.

Midpoint

The computed center between bid and ask, useful as a reference price but not proof that an order would fill.

Quote/trade condition

The condition-code, exchange, correction, sequence, and timestamp context that explains how a quote or trade row can be used.

Quote vs trade semantics

The distinction between executable bid/ask markets, printed transactions, and bar-level summaries.

REST snapshot

A reproducible request for current or historical market state, used for initialization, backfills, and audit logs.

WebSocket stream

A persistent live connection that needs subscription topics, reconnect tracking, freshness labels, and REST repair paths.

Entitlement gate

The product, plan, quote, live, delayed, historical, or commercial-use boundary checked before data is shown.

Quote freshness

The age, timestamp, and live or delayed state of a bid/ask record before it is used in a scanner, backtest, or UI.

Timestamp semantics

The exchange, provider, ingestion, session, and application time context attached to a market-data record.

Pagination cursor

The continuation token or next URL that keeps large chains, trades, quotes, and historical windows complete.

FAQ

Related questions

What makes historical options event studies unreliable?

Common problems include selecting contracts from a modern chain, using stale last price as a fill, ignoring quote age and spreads, and hiding missing-data rejects.

What should an options event replay publish?

It should publish event timestamps, exact OCC contracts, quote windows, fill rules, trade context, IV changes, spread checks, and rejected contracts with reasons.

Written by

Daniel Ratke

Research & Engineering

Daniel covers the deeper research notes: options backtesting, execution realism, robustness testing, data engineering, and strategy validation.

Product links

Build the workflow with CuteMarkets

This article is part of the broader CuteMarkets product and research stack. Use the landing pages below to move from the blog into the specific API workflow you want to evaluate.

Historical Options Data API

Use contracts, quotes, trades, aggregates, and expirations for historical research.

Historical Options Replay Runbook

Follow the knowledge-base runbook for event timestamps, quote windows, and rejects.

Options Backtesting API

Connect historical data to fill assumptions, stale-contract prevention, and artifacts.

NVDA Earnings Replay

See a concrete quote-aware replay style around a high-attention earnings event.