Daily Expirations Are Eating the Options Calendar

Viktoria Chapov

Product & Education

Daily Expirations Are Eating the Options Calendar

Daily expirations make the options calendar part of the execution system. Developers should query listed dates, select exact contracts, validate quote freshness, enforce spread filters, and preserve reject reasons before trusting 0DTE results.

Term map

Options-data vocabulary for this article

Read chains, contracts, quote freshness, trade tape context, Greeks, implied volatility, open interest, and entitlement gates as separate data objects. That vocabulary keeps an options-data workflow precise when it moves from docs to scanners, dashboards, and historical research.

Follow the linked definitions for Option chain snapshot, Contract snapshot, Volume/OI pressure, Options flow false positive, Scanner artifact, Historical REST window, Backfill, DTE bucket, Moneyness band, Quote condition, Trade condition, and IV skew.

Read this article with Options Data API, Options Chain API, Historical Options Data API, Options Volume and Open Interest, Options Flow False Positives, and Option Quote and Trade Conditions.

Cboe started offering daily expirations for Dow Jones Industrial Average Index options on May 18, 2026. The announcement says DJX options now have contracts expiring every trading day, and it frames the expansion as a response to demand for short-dated index options strategies. Cboe also reported that 0DTE trading represented a record 50.11% of all index options trading on its options markets in the first quarter of 2026. The source is Cboe's DJX announcement.

That is the market-structure hook. The developer lesson is broader: daily expirations turn the options calendar into live infrastructure. A backtest or scanner that treats expiration dates as a static weekly list will keep breaking as more products add daily, weekly, end-of-month, holiday-adjusted, and product-specific cycles.

Short-dated options are more than a strategy category. They are a data-quality test.

The launch also sits inside a broader volume backdrop. Cboe's Q1 2026 options industry review described record-setting activity across major index, ETF, and single-stock contracts. Daily-expiration infrastructure is not being built for a tiny corner of the market. It is being built into a market where short-dated option flow is already a primary workflow for many traders.

What changed

DJX options are based on 1/100th of the Dow Jones Industrial Average. Cboe's May 18 announcement added Monday-to-Thursday P.M.-settled DJXW expirations alongside existing Friday weekly contracts and third-Friday A.M.-settled monthly contracts. Cboe also noted that DJX options trade from 9:30 a.m. ET to 4:15 p.m. ET.

The exact product details matter if you trade DJX. But even if your workflow focuses on equities and ETFs, the change shows the direction of travel. Daily expirations are spreading across index products. Retail brokers and active traders are building more workflows around same-day exposure. Data systems that once got away with hard-coded calendars now need to prove that a contract actually exists before a strategy tries to trade it.

This is the practical shift:

| Old shortcut | Why it breaks |

|---|---|

| "Weekly options expire on Friday." | Many products have Monday, Wednesday, Friday, daily, or holiday-adjusted cycles. |

| "0DTE means SPX." | 0DTE behavior now appears across more index and ETF workflows. |

| "The chain is enough." | The chain is a snapshot; the replay still needs timestamped quotes and trades. |

| "Expiration date is a UI filter." | Expiration date is a core part of contract identity and strategy feasibility. |

| "No-trade days are simple." | Holidays, early closes, and global trading hours can change session shape. |

The calendar is not metadata anymore. It is part of the execution model.

Why daily expirations matter

Daily expirations let traders express very narrow views:

- intraday directional exposure

- event hedges

- short premium around a specific session

- income strategies that avoid overnight risk

- tactical index exposure with smaller calendar windows

- post-news volatility decay

That sounds like a strategy opportunity. It is also a data problem. The shorter the contract life, the more every timestamp matters. A stale quote that is harmless in a 45-DTE study can dominate a 0DTE result. A spread that looks small in dollars can be massive as a percentage of premium. A one-bar timing error can move the contract from viable to worthless.

Daily expirations compress the whole research problem into a single session.

The first data problem: listed expirations

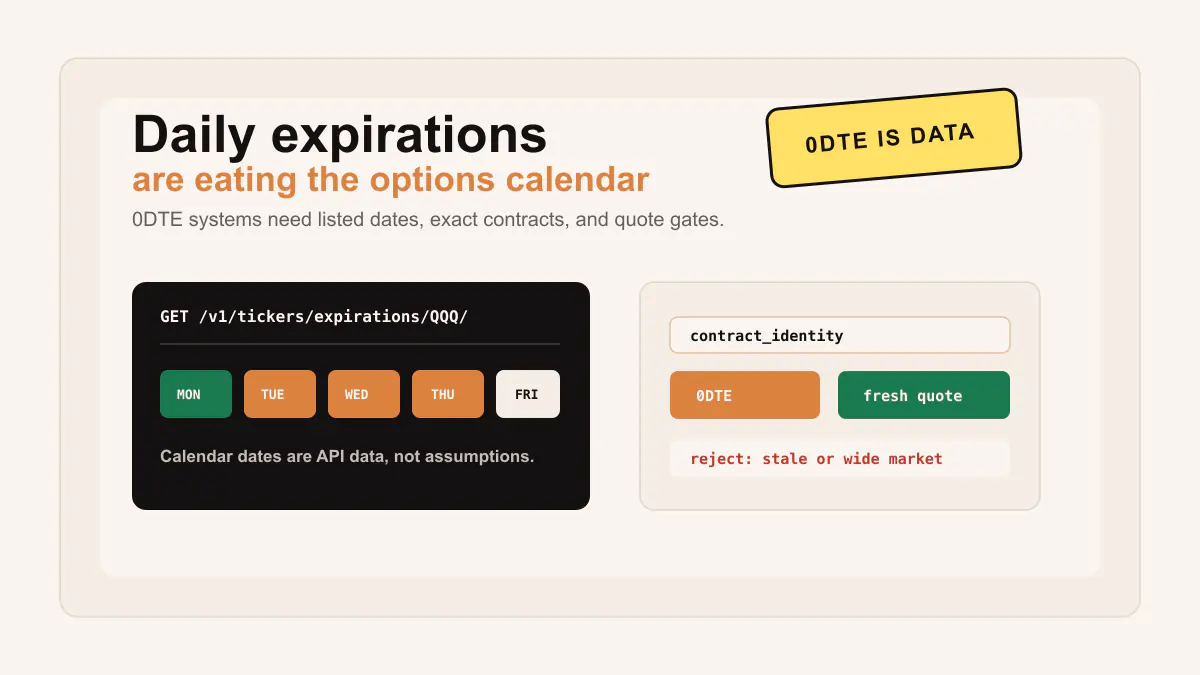

Every short-dated workflow should begin by asking which expirations are actually listed for the underlying. Do not infer the date from a calendar. Query it.

curl "https://api.cutemarkets.com/v1/tickers/expirations/SPY/" \

-H "Authorization: Bearer YOUR_API_KEY"

For ETF workflows, this prevents a common mistake: assuming every Friday or every trading day has the contract the strategy wants. Some products have broad weekly coverage. Some do not. Holidays can shift expiration behavior. Product-specific listing rules can change. The API response should decide which dates are eligible.

After expiration discovery, load the candidate contracts:

curl "https://api.cutemarkets.com/v1/options/contracts/?underlying_ticker=SPY&expiration_date=2026-05-22&limit=1000" \

-H "Authorization: Bearer YOUR_API_KEY"

That request turns the abstract date into a contract universe. The backtest can then select strikes, calls, puts, and spreads from the returned symbols instead of generating OCC strings from assumptions.

The second data problem: contract identity

Daily expirations make contract identity more important because there may be many nearby expirations with similar strikes. A strategy that accidentally selects Friday when it meant Wednesday is not slightly wrong. It is trading a different instrument.

A safe selector should store:

| Field | Why it matters |

|---|---|

underlying_ticker | The root instrument, such as SPY, QQQ, DIA, or another supported underlying. |

expiration_date | The actual listed date selected by the API. |

contract_type | Call or put. |

strike_price | The strike selected from the point-in-time universe. |

options_ticker | The exact OCC-style contract identifier used for quotes and trades. |

selection_timestamp | When the contract was chosen. |

selection_reason | ATM, delta target, spread candidate, volume rank, or another explicit rule. |

This record is boring by design. It is the artifact that stops a replay from drifting between dates, strikes, or instruments.

The third data problem: timestamp causality

0DTE research often fails because the simulator observes too much before it enters. A completed 5-minute bar should not give the strategy a fill inside that same completed bar unless the system modeled a standing order that existed before the bar closed.

For daily-expiration strategies, write the event order explicitly:

- Regular session opens.

- The strategy waits for a completed observation window.

- The signal timestamp is recorded.

- Contract selection runs using only information available at that timestamp.

- A quote window after the decision timestamp is loaded.

- The fill policy accepts or rejects the quote.

- Exits are evaluated with the same timestamp discipline.

This sequence matters more as DTE approaches zero. A few minutes can change delta, gamma, spread width, and exit availability.

The execution problem: quote freshness

Short-dated options can trade heavily, but not every line is liquid. A data system should treat quote freshness as a gate, not as a nice-to-have diagnostic.

curl "https://api.cutemarkets.com/v1/options/quotes/O:SPY260522C00600000/?timestamp.gte=2026-05-22T13:30:00Z×tamp.lt=2026-05-22T20:00:00Z&limit=1000&sort=timestamp&order=asc" \

-H "Authorization: Bearer YOUR_API_KEY"

That kind of quote window lets the fill model ask:

- Was there a bid and ask after the signal?

- Was the quote close enough to the decision timestamp?

- Was the spread below the strategy's maximum?

- Was there displayed size on the side the strategy needed?

- Did the market disappear before the exit?

- Did the contract become zero-bid before the planned close?

Those questions should decide whether a simulated trade exists. A scanner may still show the contract. A backtest should reject it if the market was not executable.

The execution problem: spread math

For short-dated contracts, a few cents can be the whole trade. A five-cent spread on a $3.00 option is different from a five-cent spread on a $0.20 option. The first is friction. The second can be the strategy.

A minimum spread policy should include:

| Rule | Example |

|---|---|

| Maximum absolute spread | Reject if ask - bid > 0.10. |

| Maximum percent spread | Reject if (ask - bid) / midpoint > 0.15. |

| Minimum bid | Reject exits where bid is zero or below a floor. |

| Quote age cap | Reject quotes older than the strategy allows. |

| Side-specific pricing | Long entries at ask, long exits at bid; shorts reversed. |

| Reprice policy | Define whether an unfilled marketable limit can retry. |

The policy should be written before the backtest sees results. Otherwise, spread filters become another optimization surface.

The calendar problem: holidays and session shape

Daily expirations make the trading calendar a runtime dependency. The week of this post is a simple example. Cboe's U.S. options hours page lists Memorial Day 2026 on May 25 with no regular trading hours. Source: Cboe hours and holidays.

A naive "next trading day" function can break in several ways:

- It can schedule a Monday strategy on a closed market.

- It can choose the wrong expiration for a holiday-shortened week.

- It can compare a regular session with a partial or unusual session.

- It can let a weekend or holiday gap leak into an intraday rule.

- It can calculate DTE from calendar days when the product's listed expirations tell a different story.

A robust system should use exchange calendars for sessions and API expiration discovery for contracts. The calendar tells you whether the market is open. The expiration endpoint tells you which option dates exist.

The scanner problem: activity is not quality

Daily-expiration markets can make scanners look busy. High volume, large premium, or fast price change can all be useful signals, but none of them proves a contract is a good candidate.

For same-day contracts, a scanner should separate activity from quality:

| Layer | Scanner question |

|---|---|

| Activity | Is volume, premium, or trade count unusual? |

| Context | Is volume large relative to open interest or normal activity? |

| Moneyness | Is the strike close enough to the underlying to matter? |

| Time | How much session time remains before expiration? |

| Liquidity | Is the bid/ask spread acceptable? |

| Freshness | Is the quote current enough to act on? |

| Follow-through | Did later quotes or trades validate the alert? |

That structure is the same one discussed in Unusual Options Activity Scanner: What Actually Matters Beyond Volume. Daily expirations make the warning sharper because the time window is shorter and the penalty for stale data is higher.

The backtesting problem: DTE is a moving object

Many backtests store a simple DTE bucket such as 0DTE, 1DTE, or 5-7DTE. That is useful, but daily-expiration products need more detail:

calendar_dtetrading_session_dteexpiration_datedays_to_last_tradesettlement_stylesession_close_timelast_trade_timeholding_period_minutes

The difference between A.M.-settled and P.M.-settled contracts can also matter. The difference between an ETF option and an index option can matter. Assignment, settlement, and closing-time rules are not cosmetic details if the strategy holds near expiration.

The safest approach is to store the product contract fields and the chosen strategy interpretation separately. Do not let "0DTE" be the only description of the instrument.

A developer checklist for daily-expiration systems

A daily-expiration data system should pass this checklist before anyone trusts its output:

| Check | Requirement |

|---|---|

| Expiration discovery | Query listed expirations before selecting contracts. |

| Contract universe | Load contracts from the API, not generated strings. |

| Point-in-time selection | Select contracts using the simulated decision date and timestamp. |

| Chain context | Capture IV, Greeks, open interest, volume, latest quote, and latest trade when available. |

| Quote evidence | Load bid/ask windows around entries and exits. |

| Trade evidence | Use prints for activity context, not as a substitute for executable quotes. |

| Reject reasons | Persist missing quote, stale quote, wide spread, zero bid, bad DTE, and missing contract reasons. |

| Session calendar | Use exchange hours for open, close, holidays, and early closes. |

| Pagination | Follow next_url until the required chain or quote window is complete. |

| Artifact output | Save selected contracts, fills, rejects, and summary metrics for replay. |

This is not overengineering. It is the minimum standard for avoiding false confidence in a market where the option can expire the same day it is selected.

How the CuteMarkets workflow fits

For supported options workflows, the core API sequence is straightforward:

# 1. Discover dates.

curl "https://api.cutemarkets.com/v1/tickers/expirations/QQQ/" \

-H "Authorization: Bearer YOUR_API_KEY"

# 2. Load contracts for a selected expiration.

curl "https://api.cutemarkets.com/v1/options/contracts/?underlying_ticker=QQQ&expiration_date=2026-05-22&limit=1000" \

-H "Authorization: Bearer YOUR_API_KEY"

# 3. Inspect the chain around the selected date and strikes.

curl "https://api.cutemarkets.com/v1/options/chain/QQQ/?expiration_date=2026-05-22&limit=100" \

-H "Authorization: Bearer YOUR_API_KEY"

# 4. Validate the selected contract with quotes.

curl "https://api.cutemarkets.com/v1/options/quotes/O:QQQ260522C00480000/?limit=1000" \

-H "Authorization: Bearer YOUR_API_KEY"

The same conceptual process applies whether the strategy is a scanner, a discretionary dashboard, or a backtest:

- Start from listed dates.

- Select exact contracts.

- Validate tradability with quotes.

- Use trades as activity evidence.

- Store rejects.

- Keep the session calendar explicit.

That is the practical answer to daily expirations. More expirations are not a problem if the system treats the calendar as data.

What this means for 0DTE content

Most 0DTE content starts with strategy rules: sell premium at the open, buy breakouts, fade extremes, hedge with spreads, avoid overnight risk. Those rules may or may not be useful. They are not the first layer.

The first layer is whether the system can answer:

- Which contracts existed?

- Which expiration was selected?

- Which quote priced the entry?

- Which quote priced the exit?

- Which contracts were rejected?

- Which session calendar was active?

- Which artifact proves the replay can be rebuilt?

If those questions are unanswered, the strategy result is not ready. If those questions are answered, the strategy can fail honestly, which is the best starting point for real research.

Takeaway

Daily expirations are spreading because traders want more precise same-day tools. That demand is real. The data burden is also real.

The more granular the expiration calendar becomes, the less tolerance a system has for shortcuts. Hard-coded Fridays, generated OCC symbols, stale last prices, and missing reject logs are survivable in toy examples. They are not survivable in serious short-dated options research.

For developers, the rule is simple: treat expiration discovery, contract identity, quote freshness, and session calendars as first-class parts of the trading system. Strategy logic comes after that.

Sources and next reads

- Cboe DJX daily-expiration announcement

- Cboe State of the Options Industry Q1 2026

- Cboe U.S. options hours and holidays

- 0DTE Options Backtesting Data Requirements

- OPEX Week Options Data: What to Measure Before Trading

- Expirations docs

- Contracts docs

- Option Chain Snapshot docs

How the terminology applies

For Daily Expirations Are Eating the Options Calendar, the options data workflow should treat Option chain snapshot, Contract snapshot, Volume/OI pressure, Options flow false positive, Scanner artifact, and Historical REST window as operational state rather than glossary decoration. That framing keeps chain selection, contract snapshots, activity filters, quote state, and endpoint access tied to the exact contract the page is discussing.

A developer implementing this Market Insight idea should persist Backfill, DTE bucket, Moneyness band, Quote condition, Trade condition, and IV skew beside the result, instead of leaving those words in a term card. It also makes false positives easier to diagnose because a high-activity contract can be separated from a tradable, timestamped, and entitled data object.

The review artifact for Daily Expirations Are Eating the Options Calendar becomes more useful when 0DTE contract, OCC root, Options data API, OPRA-originating data, OCC option symbol, and Bid/ask spread appear in the same body of evidence as the selected rows. When the article moves from concept to implementation, these fields should shape request order, cache boundaries, row labels, and review tables.

In production notes for this options data workflow, Midpoint, Quote/trade condition, Quote vs trade semantics, REST snapshot, WebSocket stream, and Entitlement gate define the checks that decide whether the workflow is reproducible. The result is a scanner or dashboard that explains why a contract was shown, skipped, refreshed, or passed into a downstream research step.

For Daily Expirations Are Eating the Options Calendar, the practical acceptance test is simple: another developer should be able to read the body, identify the exact inputs, reproduce the request sequence, and explain the accepted and rejected rows without relying on the bottom terminology grid. If a phrase appears in the page vocabulary, it should correspond to a stored field, a validation check, a replay step, or an implementation decision in the options data workflow.

This is also the reason the article should not measure success only by the final chart, table, or headline metric. The better standard is whether the data path, timing model, entitlement state, and evidence trail survive review. When those pieces are written directly into the body, the terminology becomes part of the workflow readers can implement.

Terminology

Market-data terms used in this article

These terms keep the article connected to the CuteMarkets knowledge base and to the exact API workflow behind the research.

Option chain snapshot

The current breadth view for an underlying across expirations, strikes, Greeks, IV, OI, quotes, and trades.

Contract snapshot

The focused one-leg view after a chain scanner or user selects an exact contract.

Volume/OI pressure

Same-day option volume divided by prior open interest, used as an attention filter rather than proof of new positioning.

Options flow false positive

A scanner row that looks meaningful but weakens after spread, quote age, event, trade, or structure checks.

Scanner artifact

The saved contract, score, volume, OI, premium, quote, trade, tag, and reject record behind an alert.

Historical REST window

A timestamp-bounded request for quotes, trades, contracts, or bars used to rebuild a past market state.

Backfill

A REST request used after a stream gap, retry, or missing cache hit to repair an interval explicitly.

DTE bucket

A days-to-expiration grouping such as 0DTE, weekly, monthly, LEAPS, or event-window contracts.

Moneyness band

The ITM, ATM, or OTM relationship between strike, contract side, underlying price, and delta.

Quote condition

A code attached to a bid/ask update that affects whether it belongs in scanners, backtests, or displayed state.

Trade condition

A code attached to a print that affects whether the last sale is regular, corrected, excluded, or only contextual.

IV skew

The shape of implied volatility across strikes or expirations, usually read with Greeks and term-structure context.

0DTE contract

An option that expires the same trading day and needs tighter spread, quote-age, and session-state controls.

OCC root

The symbol root inside the OCC option identifier, which can differ from casual ticker text in adjusted or special cases.

Options data API

The product surface for chains, contracts, quotes, trades, aggregates, Greeks, IV, open interest, and expirations.

OPRA-originating data

The U.S. listed-options source context behind quotes, trades, exchange participation, and consolidated option-market records.

OCC option symbol

The exact option contract identifier that preserves root, expiration, call or put side, and strike.

Bid/ask spread

The execution interval between bid and ask that determines whether a contract is realistically tradable.

Midpoint

The computed center between bid and ask, useful as a reference price but not proof that an order would fill.

Quote/trade condition

The condition-code, exchange, correction, sequence, and timestamp context that explains how a quote or trade row can be used.

Quote vs trade semantics

The distinction between executable bid/ask markets, printed transactions, and bar-level summaries.

REST snapshot

A reproducible request for current or historical market state, used for initialization, backfills, and audit logs.

WebSocket stream

A persistent live connection that needs subscription topics, reconnect tracking, freshness labels, and REST repair paths.

Entitlement gate

The product, plan, quote, live, delayed, historical, or commercial-use boundary checked before data is shown.

FAQ

Related questions

Why do daily expirations matter for options data systems?

They make hard-coded weekly calendars unsafe. A strategy must discover listed expirations, verify contract identity, and use timestamped quotes before selecting or replaying same-day contracts.

What should a 0DTE backtest validate first?

It should validate the listed expiration, exact contract universe, session calendar, quote freshness, spread width, bid availability, and reject reasons before calculating PnL.

Written by

Viktoria Chapov

Product & Education

Viktoria writes the approachable side of CuteMarkets: product updates, practical tutorials, market context, and beginner-friendly API workflows.

Product links

Build the workflow with CuteMarkets

This article is part of the broader CuteMarkets product and research stack. Use the landing pages below to move from the blog into the specific API workflow you want to evaluate.

Beginner options path

Send newcomers to the beginner path for calls, puts, chains, Greeks, IV, and risk.

Options Data API

See the main options overview for real-time and historical options data.

Historical Options Data API

Inspect the historical contracts, quotes, trades, and aggregates workflow.

Options Chain API

Go straight to chain snapshots, expirations, and strike discovery.

Pricing

Review plans before you move from free evaluation into production usage.